-

August 30, 2021

-

Directors & Officers insurance protects leaders from personal losses and can also cover the legal fees and costs the company may incur in the event of a lawsuit. Choosing the right underwriter requires a storyteller’s talent.

Every company has a story to tell. The ability to craft yours well, and back it up with sound analytics, has proven to be beneficial when negotiating with underwriters for directors and officers (D&O) insurance.

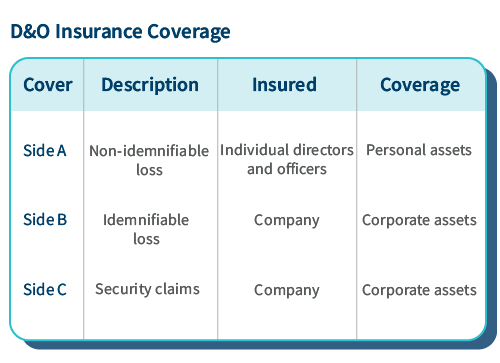

As seen in the chart below, D&O insurance provides indemnified and non-indemnified coverage to insured people’s managers from personal losses stemming from actions they take in the performance of their contractual duties. A D&O policy also covers losses associated with lawsuits, including defense fees, while typically excluding fraudulent or other criminal acts.

In this era of increasing event-driven litigation (e.g., lawsuits stemming from cyberbreaches, product recalls, social justice movements, etc.), effective D&O policies and appropriate limits can provide needed peace of mind to your board members. Coverage varies by organization: Publicly traded companies typically procure larger limits than do closely held firms. Financial profile, industry, operations and myriad other factors can impact the type and amount of D&O coverage that a firm sources.

Private equity firms also covet effective and efficient D&O insurance. Among other advantages, a policy can protect the firm and individuals against claims of breach of fiduciary duty. That’s a major selling point for investors as more PE firms access public markets via initial public offerings (IPO) or engage in special-purpose acquisition company (SPAC) markets.

But acquiring or renewing a D&O policy that best fits your company’s needs these days is not a simple task. Driven by the above scenarios and others, the cost for D&O insurance has risen dramatically since 2018. According to S&P Global Ratings,1 direct premiums in the D&O commercial line rose by 40.9 percent year over year in 2020. Among the top 20 underwriters, written premiums jumped by 41.4 percent.

Underwriters are feeling the squeeze of years of mounting losses. In addition to raising premiums and retention points, they are reducing limits, or potential payouts, in the layers of excess protective coverage that typically make up a tower and provide savings for both carriers and insured. There is little to no pricing differential among excess layers today. Additionally, program layers are now built in $2.5 million or $5 million compared to the historic layer participation of $10 million or $15 million.

Make no mistake, underwriters want your business, but given the current pricing environment, they are being inundated with submissions from insured individuals. To compete, you must press your broker to do some serious shopping around. And to stand out from the crowd, you need to be ready to make your case directly to prospective underwriters by crafting a unique story about your company’s financial and compliance position with key differentiators relative to your competitors.

Your Broker’s Role in the Story

How is your relationship with your broker? That’s important to consider early in the renewal process. You want to be able to have a frank conversation and push them at times if needed. Brokers are feeling the squeeze and the fatigue of a hardening D&O market, too. They may be tempted to simply suggest renewing an existing policy to avoid the effort — yet again — of going through another D&O marketing process that yields little impact.

Get a head start on the renewal process by at least 120 days with a renewal strategy meeting. Sit down with your broker to review your purchase limits relative to your industry and your loss profile — they will have this benchmarking material. It’s important to take a deep dive into these analytics to position your company accurately and not simply rely on a general market update. Historical loss models, particularly in the face of rising prices, may be outdated. So carefully review limit and retention points to ensure they meet your current risk appetite.

Set a timeline for the entire renewal process and execution — you want to be able to review and complete submissions with your broker before scheduling meetings with respective underwriters. Your mutual goal is to have all options for policy renewal ready at least two weeks prior to expiration.

Casting Your Underwriter

Underwriters are asking more questions early in the process about performance, and their expectation of transparency is high. In fact, the more transparent and complete your submission is, the greater the likelihood an underwriter will take the time to fully vet your submission and the associate pricing.

The key here is creating a "best-in-class" underwriting story. You’ll need to have a clear message about the following emerging topics:

- COVID response and performance/execution post-lockdowns

- Financial condition and debt maturity table

- Claim and litigation history

- Harassment and awareness training and compliance, especially for senior managers in the wake of #metoo and social justice trends

- Cyber posture, including annual IT investment and preparedness for ransomware losses, together with protection and procedures

- Retirement plan fiduciary responsibilities

Strong, overt messages about all of the above are critical; anything perceived as missing or insufficient will lead underwriters to assume your firm lacks structure around them. The outcomes can be costly: As the old axiom goes, "underwriters plug holes in submissions with premium dollars."

For soon-to-be-public companies, board composition and public company experience are also major components of your story. If your firm or private equity sponsor is recruiting a public company board, be sure there is sufficient coverage of the members themselves, as well as the respective representation on key committees, including audit, compensation, governance and finance.

The Final Chapter

Pricing for D&O insurance is not expected to decline in the near future. Potential fallout stemming from the COVID-19 pandemic is expected to affect costs and squeeze underwriters further. Lawsuits against firms in hard-hit industries such as airlines, healthcare and hotels may increase — particularly so given the debt burdens required as they navigate the effects of the lockdowns last year. Shareholders may sue companies over financial performance.2

On the positive side, the pandemic normalized the use of videoconferencing across industries, allowing more opportunities to present your story directly to underwriters with all bodies present, including your broker. A virtual meeting offers the moment to speak from the heart with the knowledge (and data) that only a company can bring.

Finding and renewing a D&O policy that fits right is truly challenging today. But it can be done. Knowing how to navigate the process and craft a thorough and compelling story with sound analytics that will impress underwriters will set you apart. It may be a long story to write, but with the right expertise the final chapter can end on a satisfying note.

Footnotes:

1: “D&O Premiums rise 41% YOY in 2020; loss ratios hold steady.” S&P Global Market Intelligence. May 5, 2021. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/d-o-premiums-rise-41-yoy-in-2020-loss-ratios-hold-steady-63997938

2: “Once coronavirus fades, global businesses are set to face new danger: a wave of lawsuits.” Fortune. Mar. 4, 2020. https://fortune.com/2020/03/04/coronavirus-global-businesses-wave-lawsuits/

© Copyright 2021. The views expressed herein are those of the author(s) and not necessarily the views of FTI Consulting, Inc., its management, its subsidiaries, its affiliates, or its other professionals.

About The Journal

The FTI Journal publication offers deep and engaging insights to contextualize the issues that matter, and explores topics that will impact the risks your business faces and its reputation.

Published

August 30, 2021

Key Contacts

Key Contacts

Senior Director